The holistic view counts: A variety of transformation drivers lead to changes that must not only be implemented and designed in the process organizations, but for which, above all, the employees must be successfully brought along. During significant changes, people go through different phases of an emotional process. That is why their targeted support and motivation are particularly important success factors for us: The will to shape and change must be encouraged, and sometimes worries or fears must be allayed. Our consultants accompany your employees as well as group dynamic change processes from the very beginning and adapt the change design we have developed according to the situation. Openness to change: Communication plays an elementary role for us to create transparency, to dissolve any resistance, to drive processes and integration. We make complex and dynamic transformation projects comprehensible and transparent. Through active participation, we ensure broad acceptance and joint identification.

What does change actually have to do with us as a consulting firm? A lot – or rather everything! Because only those who remain open to new things, constantly question themselves as consultants and reflect on their own actions can drive change and initiate creative solutions.

Our systemic approach helps us to perceive and shape dynamic processes. We create space for trust, for participation and provide orientation for alternative solution options. In doing so, our view is always appreciative and solution-oriented. Learning never stops for us and shapes our corporate culture: For Consileon, the focus is not only on individual learning, but on learning from each other. Through reflection work, we become more aware of our own abilities and can use them in a more goal-oriented way. We train our consultants both internally and externally. We are not primarily concerned with obtaining certificates and degrees. The focus is rather on the concrete application and (experience) of an agile and systemic way of thinking and acting. We see this as a clear added value for our customers.

If you want to actively tackle change, you need new ways of thinking and innovative tools. In an extremely dynamic and complex environment, mechanistic methods and traditional ways of working according to sequential linear steps towards a predefined solution no longer work. Effective approaches and tools like these have long been our method:

Learn more in our brochure on Change Management and Agile Transformation. (*only available in German)

We help you turn legislation into innovative services. Take the Central Securities Depository Regulation (CSD Regulation), for example. What does this have to do with you? More than you might think: Anyone who trades securities will have to deal with the regulation, and the rules differ depending on the type of security and the trading venue. A central securities depository (CSD) is an entity that stores financial instruments such as stocks or bonds for holders or their banks, respectively, and provides ancillary services. If a seller defaults on a transaction with a CSD, he or she will also be subject to sanctions in the future if the transaction is not conducted via a central counterparty (CCP), such as a clearing house. In addition, market participants from the EU must appoint a neutral buy-in agent as an alternative supplier of the security in the event of default. Participants working with an external buy-in service comply with this legal obligation and mitigate any penalties.

Do you operate a global depository with a large network of depositories? Then you could also act as a buy-in agent for the traders and brokers among your clients.

Consileon combines industry knowledge with change management expertise. In order to hold one’s own on the market, it is not enough to awaken latent needs via digital marketing. Design thinking experts develop digital products the way the target groups want them.

Together with your team, we formulate use cases that you can coordinate with customers and business partners of your market platform. Using an agile approach, we quickly determine how product ideas are received by the target groups, so that you only develop the best ideas to market maturity and avoid expensive bad investments. To accomplish all this, Consileon’s capital market experts and accomplished change managers work hand in hand.

“Design is not just how it looks and feels. Design is how it works.”

Steve Jobs (co-founder Apple)

The theory of constraints assumes that there is always exactly one bottleneck in a company that determines the performance of the whole. It is therefore essentially a matter of identifying this bottleneck and, if possible, eliminating it.

Below you will find an exemplary roadmap for the implementation of portfolio optimisation by means of bottleneck management.

With industry knowledge, analytical strength, strategic thinking and innovative power, we help companies in the insurance industry to master the challenges of a market in transition.

Together with our clients, we develop sustainable solutions for all links in the value chain: from product development to marketing, sales and risk management to IT. To deliver an immediately usable result, we provide you with consulting, software and project work from a single source.

Our core competencies include consulting on sales topics. One focus is the optimisation of processes and IT systems for the cooperation of insurers with their sales partners. Here, the following tasks, among others, have to be solved:

The insurance market is largely saturated. Customers are becoming more critical. Before signing a contract, many inform themselves via comparison portals or on interaction platforms (social media) on the internet. In addition, providers of substitute products such as bank or fund savings plans are increasing the competitive pressure.

Demographic change and changes in the preferences of potential policyholders require a revision of product policy and distribution. Offers must be reviewed in terms of their benefits for the customer, differentiated and repositioned. For example, instead of a rigid tariff scale, consumers today would rather have a modular system of basic and additional modules from which they can individually compile their insurance cover.

Direct sales via the Internet are gaining in importance, especially in the business with standardised services such as supplementary health, liability or property insurance. But products requiring advice can also be marketed online – for example by means of cobrowsing or chat functions on the provider’s website. Younger customers in particular also expect to be able to carry out simple actions such as reporting a claim via a mobile device.

Sales through banks, brokers and financial product distributors continue to increase at the expense of exclusivity. In order to leverage synergies and boost sales, it is necessary to develop an overarching marketing strategy including sales management, to network the sales channels and to support the sales partners according to their value contribution. This includes the introduction of a remuneration model that avoids conflicts between sales targets, advisory quality and compliance.

Opportunity and risk are the two sides of the same coin. If you want to make profits, you have to invest. And in doing so, you automatically take risks. However, the occurrence of excessive risks can not only ruin entire companies, but escalate into a systemic crisis. The accumulation of such crises prompts legislators to intervene.

Due to the still lingering crisis of 2008, the financial industry has been under regulatory pressure for years, especially in the USA and Europe. This particularly affects risk management. There is no end in sight. The relevant legal standards have an impact at both strategic and operational levels. Their influence extends from the business model to organization, functions, processes and methods, right through to technology and corporate culture.

Whether setting up, expanding or restructuring risk management, whether a detailed issue or a major project: financial institutions that want to keep risks under control in line with regulatory requirements find a competent, pragmatic partner in Consileon. We help our clients not to be overwhelmed by the regulatory tsunami, but to surf ahead of the wave, always towards success. Especially in risk management, it is important that all hands interlock. Partial aspects can be tackled individually, but the results must be coordinated and integrated into the big picture. This makes risk management a task that is as exciting as it is comprehensive. Among the factors on the radar of the supervisory authorities are the following:

Our interdisciplinary teams of consultants help financial intermediaries analyze and map the above factors in line with regulatory requirements. In addition to financial risks, our project practice covers other risk types including risks in cross-cutting functions, including:

Are you looking for a loyal partner who can provide you with advice and support for risk management initiatives? Then we look forward to receiving your inquiry.

The business of asset managers has changed dramatically over the past ten years. Only the respective market leaders benefit from the triumph of passive products. The clients of active asset managers are becoming more demanding, the sales structures more complex.

The financial crisis is also a crisis of assets under management. In the coming years, asset management and its distributors must demonstrate that their products deserve the trust of investors. To do this, they need to position themselves clearly in the market: either through exposure to liquid markets at a low price (cheap beta) or with high value contributions through active management (expensive alpha). In both models, market success stands and falls with the quality of the support provided to clients and distribution partners. For asset managers, this results in an extensive agenda. In addition to products, distribution partnerships are being put to the test and new sales channels are being opened up. Investors have access to information around the clock, and complementary services such as risk management are increasingly being marketed as stand-alone services. In Consileon, asset managers find a competent partner who sees change as an opportunity. We advise our clients on topics such as:

In anticipation of persistently low interest rates and rising inflation, professional management of their assets is becoming more important to investors. To benefit from this trend, providers must convince with attractive products, first-class service and sustainably low costs. Consileon supports them in this with:

The optimization of business processes requires a critical inventory of the system landscape. As an experienced partner, Consileon supports asset managers in modernizing their IT with the following services, among others:

In den letzten zehn Jahren hat Consileon acht Kundenbindungsprogramme maßgeblich mitkonzipiert, weiterentwickelt und betreut, davon sieben allein in den letzten drei Jahren. So unterschiedlich die hierbei betreuten Kunden sind, so unterschiedlich sind auch diese Kundenbindungsprogramme: stand-alone oder partner-übergreifend, mit Anmeldung oder anonym, mit oder ohne Karte, online, mobile oder papiergebunden.

Meine Übersetzung

So leisteten wir im letzten Jahr für unsere Kunden über 1.200 fachliche und über 2.300 technische Beratertage in 30 Handelsprojekten, betreuten dabei insbesondere 15 Kernsysteme unserer Kunden.

Die hierbei angepassten bzw. neu konzipierten Systeme realisierten hierbei bis zu 3.000 Handelskampagnen p.a., verarbeiteten bis zu 630 Mio. Bons p.a. von bis zu 46 Mio. Loyalty-Kunden, prüften und lösten hierbei bis zu 4 Mio. Coupons am Tag ein, kommunizierten real-time mit bis zu 30.000 Kassen und 7.000 Service-Terminals in 7.000 Märkten bzw. bedienten bis zu 100.000 aktive Online-Kunden am Tag, dabei wurden Verarbeitungszeiten von kassenbedingten Transaktionen von unter 58 ms in 98 % der Fälle erreicht.

So unterschiedlich die Systeme sind, so unterschiedlich sind die eingesetzten Technologien: JAVA, .NET/C#, MS Dynamics AX, JS, Angular, SAS (CI, MOM, RTDM), SAP, OSIS, ARC, MQS, Kafka, Hadoop (Cloudera, MapR), APM, Azure DB, IBM DB/2, MS SQL Server, Oracle, Teradata, BigData, AzureCloud, GoogleCloud, SpringBoot, Windows 7, Windows 10, Solaris, LINUX, AIX, MVS, SpringAOP,…

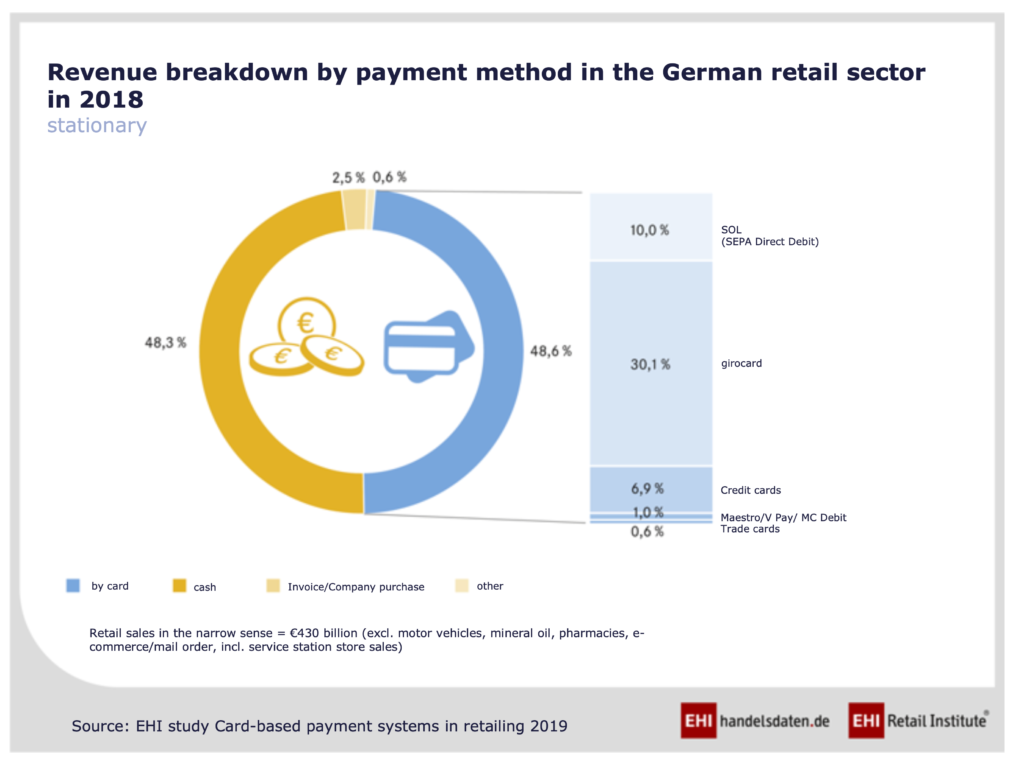

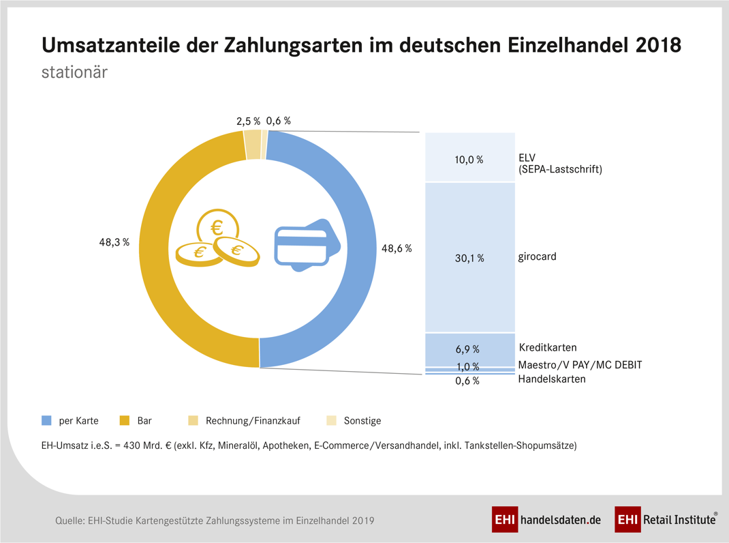

Several years behind European neighbors such as Denmark, Sweden and the Netherlands, mobile payments have now also arrived in Germany. Driven by the large, mostly American card companies and tech groups, retailers, banks and network operators have upgraded the payment infrastructure and developed processes that are gaining acceptance among the public. At the beginning of 2018, only one in five people made contactless payments by bank card, credit card, smartphone or smartwatch; according to a Postbank study, this figure rose to one third within a year.

The advance of contactless payment is likely to continue, especially as more and more banks are supporting systems such as Apple Pay and new players such as Bluecode are establishing themselves on the market. This is also supported by the declining share of cash payments in sales, which fell below card sales for the first time in 2018 at 48.3 percent.

In light of the trend, merchants should examine how payments can strategically support the core business. The following aspects are critical:

For several years now, more and more German retailers have been offering the Chinese payment service Alipay at the checkout, including the drugstore chain “dm” since summer 2019. Drugstore goods made in Germany are popular in China. The payment option is aimed on the one hand at tourists, and on the other at Chinese living in Germany who shop for addressees in the People’s Republic.

Before the Corona crisis, Alipay expected a good 160 million international trips from China in 2020. With the retrofitting of payment methods that appeal to new target groups, stationary retailers are standing up to the web stores. In addition to international services, including Alipay or its competitor WeChat Pay , these include innovative processes such as the data-saving Bluecode or cash payments for online purchases at the store checkout.

According to the market research firm Nielsen, the number of store visits in Germany fell from 232 to 193 between 2013 and 2018. The lower the frequency of visits, the more important it becomes to offer customers goods or services that interest them on that very day with every purchase. As the share of electronic payments increases, so does the amount of customer data that can be analyzed to formulate such offers relevant to that day. Tech company Apple, for example, in December 2019 refunded shoppers who paid with the company’s own credit card six percent of the price of goods instead of the usual three percent. Amazon and the Payback bonus system also analyze the virtual receipt in order to encourage customers to make further purchases with offers tailored to content and time.

According to the industry newsletter Finanzszene, Germany’s most profitable bank in 2017 was the finance subsidiary of the VW Group. So if a carmaker is raking in hefty profits with financial services, retail companies should also consider whether setting up a finance division might not be more lucrative than depending on external service providers who are primarily pursuing their own self-interest.

The recast of the EU Payment Services Directive (PSD) facilitates market entry for new players and enables real companies to offer financial services that support their core business. The advantage of this approach lies in the strong alignment of such services with the real economy business model.

While pioneers like the Otto Group failed with Yapital, the chances of success are much better today due to the greater acceptance of mobile payment. The Payback Pay system, for example, which like Yapital operates with QR codes, has established itself on the market.

For years, mobile payment specialists in retail had their hands full with the implementation of regulatory and operational requirements. Now there is more time to drive innovation at the checkout.

Within the Consileon-Group, aye4fin advises DAX-listed companies and start-ups on the topics of electronic payments, e-commerce platforms and data analysis. With profound experience from projects at domestic and international market leaders, the colleagues help design, operate and optimize the relevant systems.