The participants in the supply chain

A decisive factor for the breakthrough of electromobility on the mass market is the development of a universal charging infrastructure that is available everywhere. In recent years, various providers have developed in this area, but there is still no perfect solution for end customers to use throughout Europe.

To understand the background and today’s challenges, it is necessary to look at the value chain of the charging infrastructure as a first step. This is defined by an orderly sequence of activities that ends when the car is charged for the end customer.

The supply chain in detail

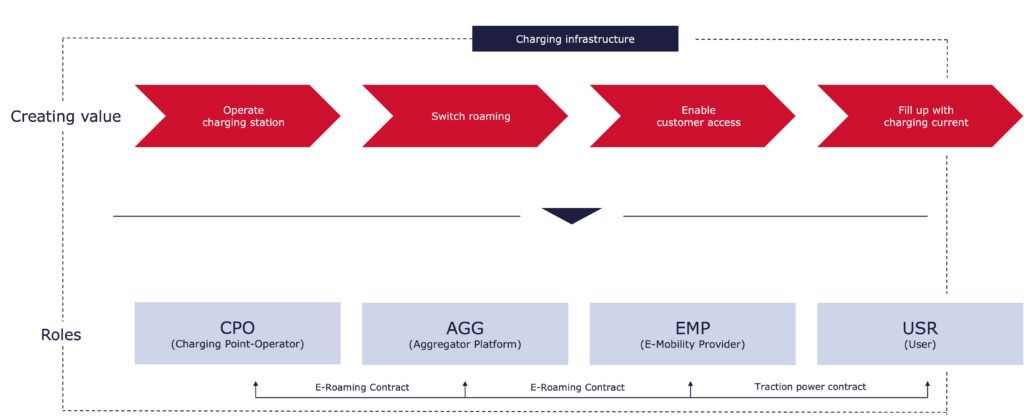

In the value chain, standardized roles have developed for the individual activities, which are largely performed by different companies. The following figure depicts the generic value chain with its assigned roles/actors, which are subsequently described.

The end customer (USR = user) purchases the service at the end of the value chain. His main goal – as familiar from the combustion engine – is to be able to use the widest possible range of charging options in the form of charging points on an ad hoc basis. To the annoyance of customers, the payment modes of the respective charging stations differ according to their operators. In addition to various payment options, they require membership and issue their own cards for this purpose.

The e-mobility provider (EMP) represents the interface between various charging station networks and the end customer. With its contractually regulated offer, the EMP enables the end customer to charge at third-party or different operators. It is not the operator of the charging points, but only offers their use to end customers. Customers pay a basic fee (e.g., €4.95 per month) and are thus also allowed to charge at partner companies. This option is referred to as e-roaming. The essential goal of the EMP is to maximize charging options for its customers – similar to what DKV does in the area of gas stations. For example, the company Plugsurfing is marketing an app that will enable payment at all charging points in Europe, regardless of operator or platform. This service works in a similar way to PayPal.

The chargepoint operator (CPO) operates its own charging stations for its end customers, but also offers its network service via a sales partner, the e-mobility provider. In this way, it also reaches end customers who are not customers of its own network. Due to the large number and variety of CPOs and their diverse, technical solutions, another role has established itself in the value chain, that of aggregator.

The aggregators (AGG) and their technical platforms represent the interface between the charging station operator (CPO) and the end customer’s contractual partner (EMP). The essential goal is to mediate charging station to e-mobility providers, in turn promoting their goal of highest network coverage. This is achieved by building a platform for different providers, such as Hubject, to implement real-time authorization of charging for end customers across providers. However, only very few providers are currently filling this role. The decisive factor for a successful business model is corresponding market power. The background to this is that the aggregator must not only have a contract with the respective partner (CPO and EMP), but also the CPO directly with the EMP.

For market entry as well as further development of the charging infrastructure, it is essential to know and understand the market participants and their different roles in the value chain.

Consileon considered and compared all European market players in the field of charging infrastructure based on the following criteria:

- Description of offer and role

- Number of charging points

- Authentication and registration of customers

- Cost model and billing

- Business area