As the use of digital access channels increases, customers are providing banks with more and more personal data. Those institutions that leverage this raw material can anticipate customer needs before they arise and contact their customers individually, with tailored solutions. Data analytics helps banks translate data into information and achieve a holistic understanding of their customers. This is made possible by innovative analysis processes that derive specific sales and consulting impulses (e.g. Next Best Offer). With this 360° view of the customer, the retail bank can develop from a standardized product provider to an individual financial coach. Customer contact and thus also sales will become highly effective thanks to technology-supported individual customer care with mass-customizable performance. The mass customization approach will prevail in the retail banking of the future.

Corporate customers are a desirable object in the currently low-margin banking sector – but only if they have top credit ratings, do not hold high demand deposits, are not subject to seasonal fluctuations, and only invest in EU member states with very good country ratings.

Low risk and commission-based business is therefore the magic formula that many banks are urgently looking for in corporate banking. In addition to a positive impact on earnings, this would also be encouraged by the regulator, which rewards this orientation with a correspondingly low capital backing. Unfortunately, however, there is significantly less demand than supply for such commitments, so that fierce competition for corporate banking business has become established in some cases. The continuing low interest rate phase, with its high impact on the achievable credit margin, is doing the rest.

In addition, customers’ expectations of corporate bank services are changing, as the increasing digitization of value chains also includes closely linked financial flows. Consileon analyses assume that around EUR 5-6 billion in revenue per year in the corporate banking business is at risk from developments in digitization. That means around 25 % of total revenues. But here, due to outdated systems and evolved structures, banks are struggling to ensure the necessary flexibility and adaptability to meet the changing market conditions. However, the up-and-coming FinTechs are already waiting in the background, and their lean structures and modern, web-based systems mean that they are now also penetrating the corporate segment.

Find out more in our Corporate Banking 2020 study.

(The study is in German.)

Corporate banking, as an essential business area for many banks, is currently not keeping pace with digitization efforts in retail banking. The use of analog processes is the reality for many business customers, who are forced to resort to browser solutions for private customers for their financial management, which do not meet their needs. For this reason, digital solutions in the areas of lending, financing, investment, and pensions and insurance in particular are a must for corporate banking in order not to miss out on the digital transformation and to fully serve the needs of business customers.

To ensure that banks remain relevant to corporate customers in the medium to long term and maintain customer loyalty, Consileon provides support in setting up and developing a high-performance platform or accompanies cooperative ventures with existing providers of such digital platforms. Key components of platforms are the presentation of the product world in corporate banking, including extensive product information, as well as the possibility of direct contact with a product expert. To enable corporate customers to purchase the desired product directly, the integration of online closing lines is required. The display of cross-selling products offers customers additional options for covering their financing needs. Further support is provided to sales thanks to the preparation of relevant information in the form of a newsletter. Corporate customers can view their products at any time and manage them via the platform.

The current business model of many corporate banks requires significant changes due to radically new regulations, technologies, customer expectations and adjusted economic conditions. Corporate banking must face the following key challenges:

With the Consileon Target Operating Model (TOM), Consileon supports banks in optimally adapting to the corporate banking of the future. This is achieved by developing a clear demand-driven strategy that focuses on the customer and describes the blueprint for building a flexible and future-proof operating model. On this basis, a transformation roadmap can be derived to bundle the ongoing but partially fragmented initiatives into a powerful program. Crucial to this is the change management competence of the corporate bank, as the frequency of the necessary adjustments is more likely to increase than decrease in the coming years.

In order to fulfill the digital wishes of corporate customers in the age of digitization, financial institutions are increasingly relying on platform strategies. The majority of banks are currently focusing more on setting up and expanding their own corporate customer platforms with small and medium-sized corporate, business and commercial customers as a key target group. At present, these often still use the classic online branch, which is more geared to private customers’ needs. Setting up their own platform helps banks to be relevant to corporate customers in the medium to long term and ensures direct, immediate contact with them. The key here is for banks to consider the extent to which their own platforms meet the modern requirements and usage habits of corporate customers. Financial service providers are currently in the process of establishing platforms to which start-ups and a wide variety of payment providers or merchants can dock.

Data analysis and data management in banking are still mainly focused on supporting internal processes. In the age of digitalization, however, customer data is critical to the success of the majority of companies and financial service providers. The essential goal is to transform into a data-driven or data-driven organization – and to consistently align with customer needs.

In corporate banking in particular, customer data can be used specifically to analyze customer needs on the one hand and demand behavior on the other. The first step involves the use of big data analytics technologies, which enable data-based decisions to be made and this data to be integrated into business processes in a way that adds value. In addition, intelligent algorithms are used to perform much more complex data analyses than before and to train and “teach” so-called machine learning systems. This means that these systems will later be able to recognize patterns and regularities in large volumes of data on their own and make autonomous decisions, for example when it comes to providing tailored investment offers or financing options for a specific corporate customer.

To improve both the quality of customer relationships and their own cost performance, corporate banks must adopt digital tools and practices more broadly and sophisticatedly. Currently, traditional corporate banking service relies almost exclusively on the acumen and interpersonal talent of relationship managers to build and deepen corporate relationships, attract customers, and drive revenue. However, this approach no longer delivers the revenue that corporate banks need in a slow-growth, low-return environment.

It’s time for enterprise banks to change the way they serve customers. They need to deploy a mix of digital and in-person services that enrich the customer experience, improve cost performance and sustain growth. Leading banks will go a step further and transform their relationship models by offering a different mix of digital and non-digital services for each customer segment: a digital self-service experience for small businesses, a hybrid human-machine offering for mid-market customers, and a highly personalized, digitally enhanced service model for large enterprises with the most demanding needs.

The growth and sustenance of the $8 trillion global trade finance market relies heavily on the ready availability and robustness of financing mechanisms. Given that trade finance is widely seen as fueling global trade, it is easy to see why blockchain is dominating the conversation in the world of trade finance.

Current trade finance is inefficient and the industry is highly vulnerable to fraud. Paper processes from our analog past urgently need to be modernized or replaced with digitized processes. Blockchain will play a major role in this transformation.

Blockchain can reduce processing time, eliminate paper usage, and save money while ensuring transparency, security, and trust. By removing bad trading partners and forcing everyone to trade fairly in a new transparent way, the risk of manipulation by chain participants is virtually eliminated.

Nowadays, companies have access to a greater variety of financing options and can put these together from loans and capital market products. Due to the increased uncertainty in global trade, the demand for letters of credit is rising in trade finance. Especially when entering new markets or doing business with new partners, the desire for innovative and customized financial solutions arises. Of correspondingly great importance is investment banking, which is closely integrated with corporate banking, in order to support customers in their day-to-day business and to develop and offer suitable solutions for their individual financing needs.

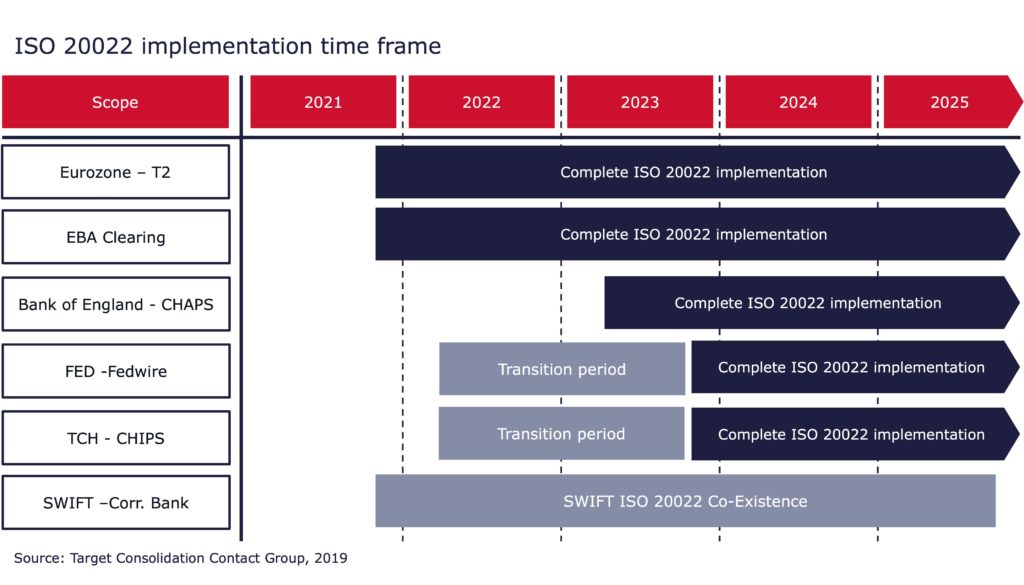

In the course of the technical and functional consolidation of the Target2 payment transaction system (T2) with the Target2-Securities (T2S) securities settlement platform, the central banks of the Eurozone (Eurosystem) will gradually introduce the ISO 20022 message standard over the next few years. Adapting to this standard will be a mammoth task for banks. A key point is the conversion of payment traffic messages from SWIFT formats (message types, MT) to XML. The long-term goal is global convergence of message standards.

Credit institutions should take this reform very seriously. Those who miss the deadlines here will literally lose out. After the changeover, it will no longer be possible to communicate with Target2 in the old formats, and the link to the ECB will be severed. As a result, defaulting institutions will not only cut themselves off from interbank clearing and from their minimum deposits, but also from favorable refinancing with the central bank. What seems to be bearable and negligible in the acute low-interest phase will take its revenge as soon as the ECB raises the key interest rate. The Swedish Riksbank has just raised its key interest rate.

In any case, the Eurosystem is one of the laggards in the switch to the XML message format. Pioneers such as the Bank of England, the Fed, the Swiss National Bank and the Japanese central bank have been making the switch for years.

In addition to format conversion, T2-T2S convergence includes the following measures:

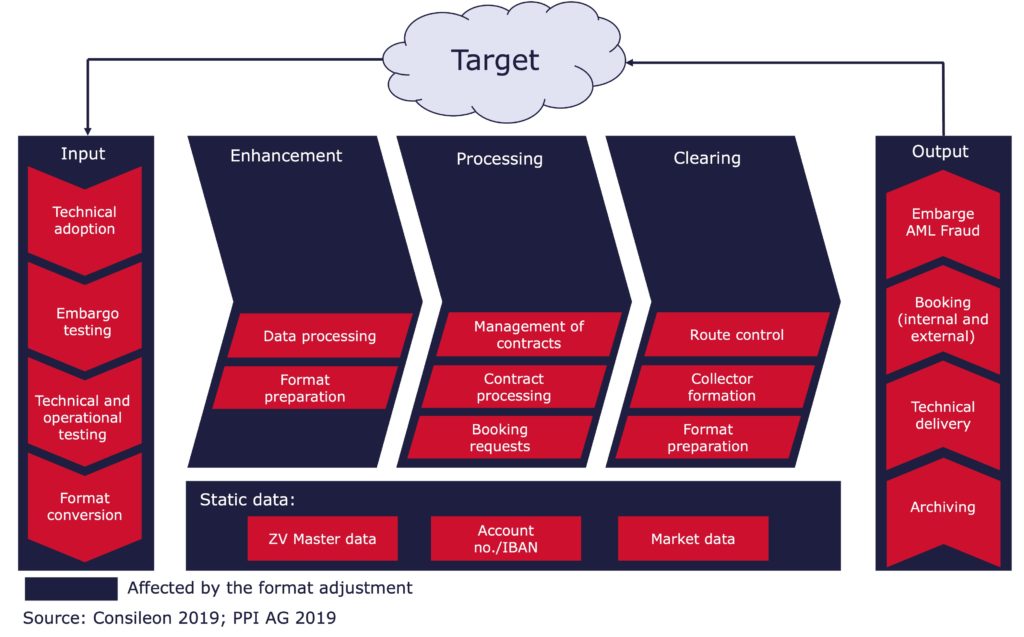

The changeover of the message format initially affects payment transactions with customers (MT1xx) and banks (MT2xx) as well as cash management and customer data (MT9xx).

Although other players such as SWIFT have postponed their releases because of Corona, the ECB is sticking to its schedule. According to this, T2 and T2S will be technically consolidated on November 22, 2021. After the “big bang,” credit institutions will have to comply with the new standard. The ECB has explicitly ruled out a transition period in which the old and new formats coexist.

Non-adapted systems, for example in payment transactions, cannot process the XML format. Each institution should therefore take stock as quickly as possible, determine its need for action and find a customized solution. We see three options here:

Each of these solutions has its advantages and disadvantages. Even if options 2 and 3 have less impact on day-to-day business in the short term, banks should not underestimate the effort involved in T2-T2S consolidation including ISO 20022 conversion.

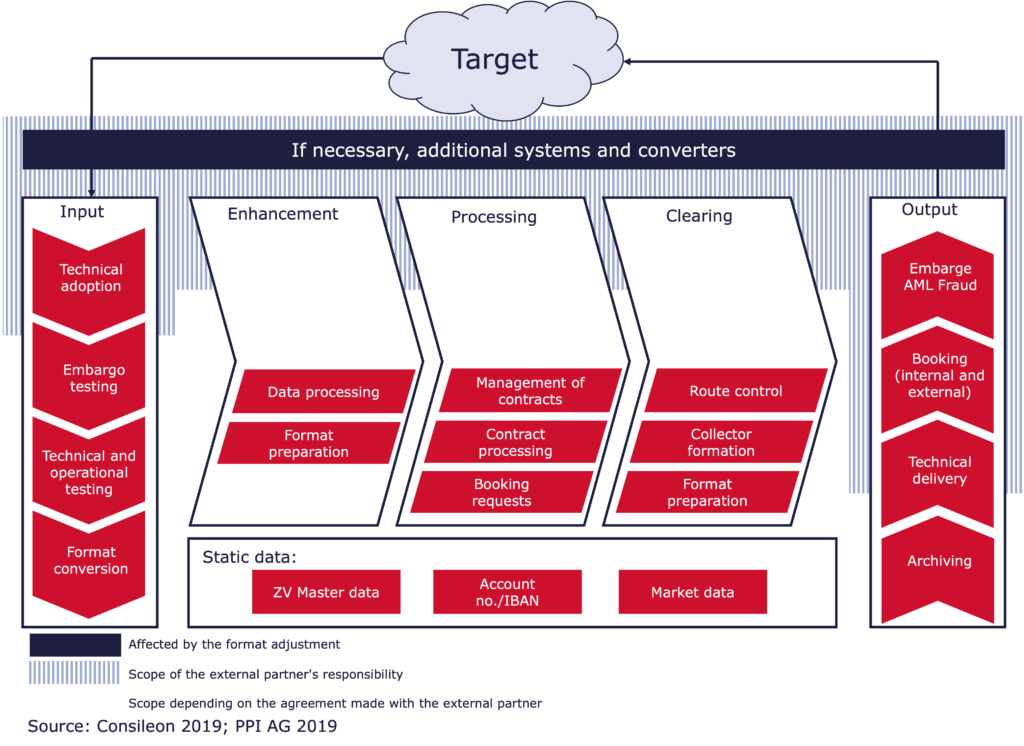

Payment messages are processed in a number of systems in banks, including account information systems, e-banking, technical archives and liquidity management. These legacy systems still operate with SWIFT messages, among other things. Urgent cross-border transfers occur not only in regular payment transactions, but also in trade finance and securities business. In addition, interoperability with anti-money laundering (AML) software and embargo checking systems must be ensured.

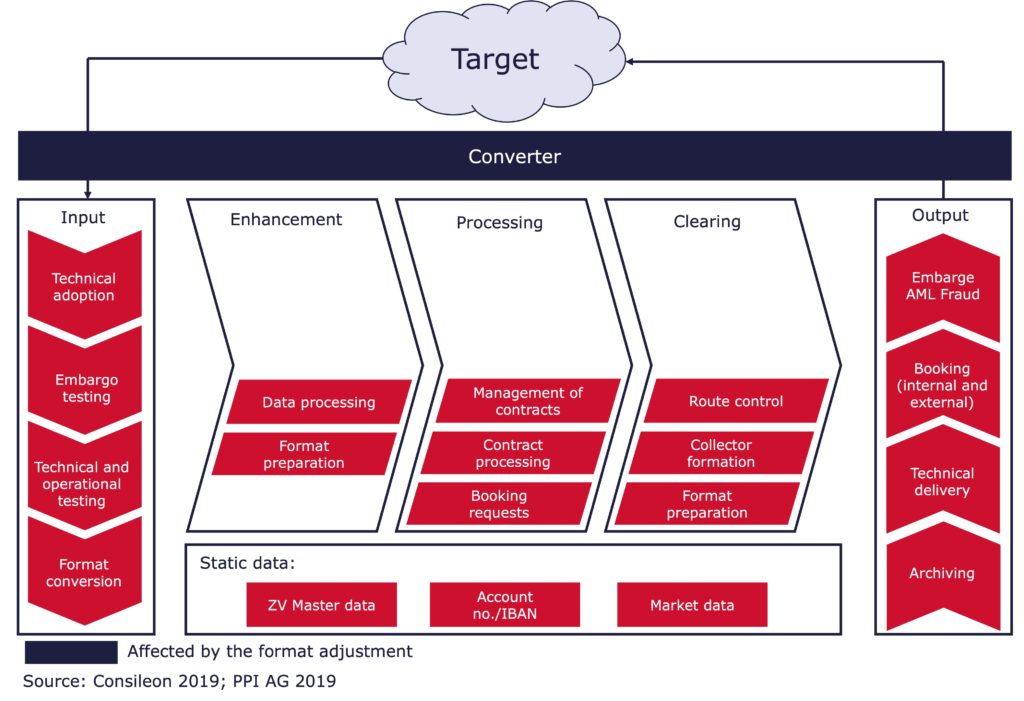

When using a converter, the legacy systems continue to work as before. The program converts incoming messages into the old format. After processing, it formats the output into XML. There are three cases to distinguish in this procedure:

To ensure that information is not lost in any of the three cases, the data fields of the incoming messages must be mapped to the internal model in advance. Overlong or new content is distributed to several fields of the internal model. If necessary, new fields are to be created. For new information that cannot be integrated into the internal data model, alternative further processing or at least archiving must be programmed. Special attention must be paid to outputs that are sent to customers, such as account statements, or that are forwarded to other institutions.

Because the data models and processes vary from institute to institute, there is no patent remedy for the use of a converter. For this reason, those responsible at the institute must analyze and regulate the three use cases in advance together with the developers and test them again and again during the course of the project

Anyone wishing to outsource payment transactions must first decide which work steps the external partner should take over. This raises similar technical questions to those relating to the use of converters. The outsourcing solution must also prevent any conceivable disruption to the flow of information. In consultation with the service provider, it must be clarified how the incoming data will enter the processing systems and how the output will be sent.

One sticking point is the external processing of orders in which the institute acts as an intermediary between several parties. If deficiencies in the outsourcing solution result in information being lost along the way, third parties may be harmed.

In the case of outsourcing, too, much depends on the circumstances at the client. For this reason, there is no standard solution here, just as there is no standard solution for options 1 and 2.

As there is no way around ISO 20022 in the long term, we recommend adapting all systems by the deadline. The new message format will become the world standard. If you want to be able to process incoming and outgoing data for payment transactions as quickly and error-free as possible in the future, you would be well advised to convert to XML messages. If time is of the essence, a converter will help you to remain capable of acting in the short term. Above all, when working out the requirements for this solution, banks gain valuable insights into their IT architecture, which they can draw on when adapting their systems natively at a later date.

Consileon provides advice and support for T2-T2S consolidation projects including ISO 20022 implementation – from evaluating options to designing processes and services.